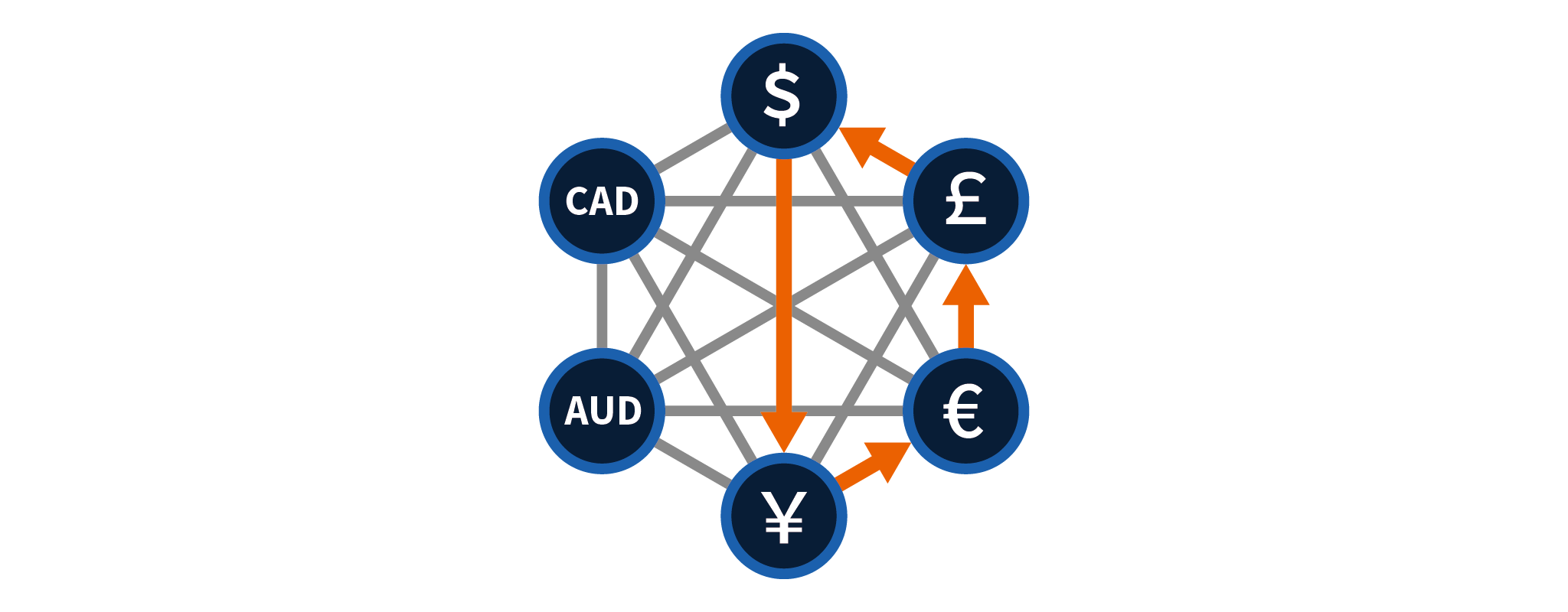

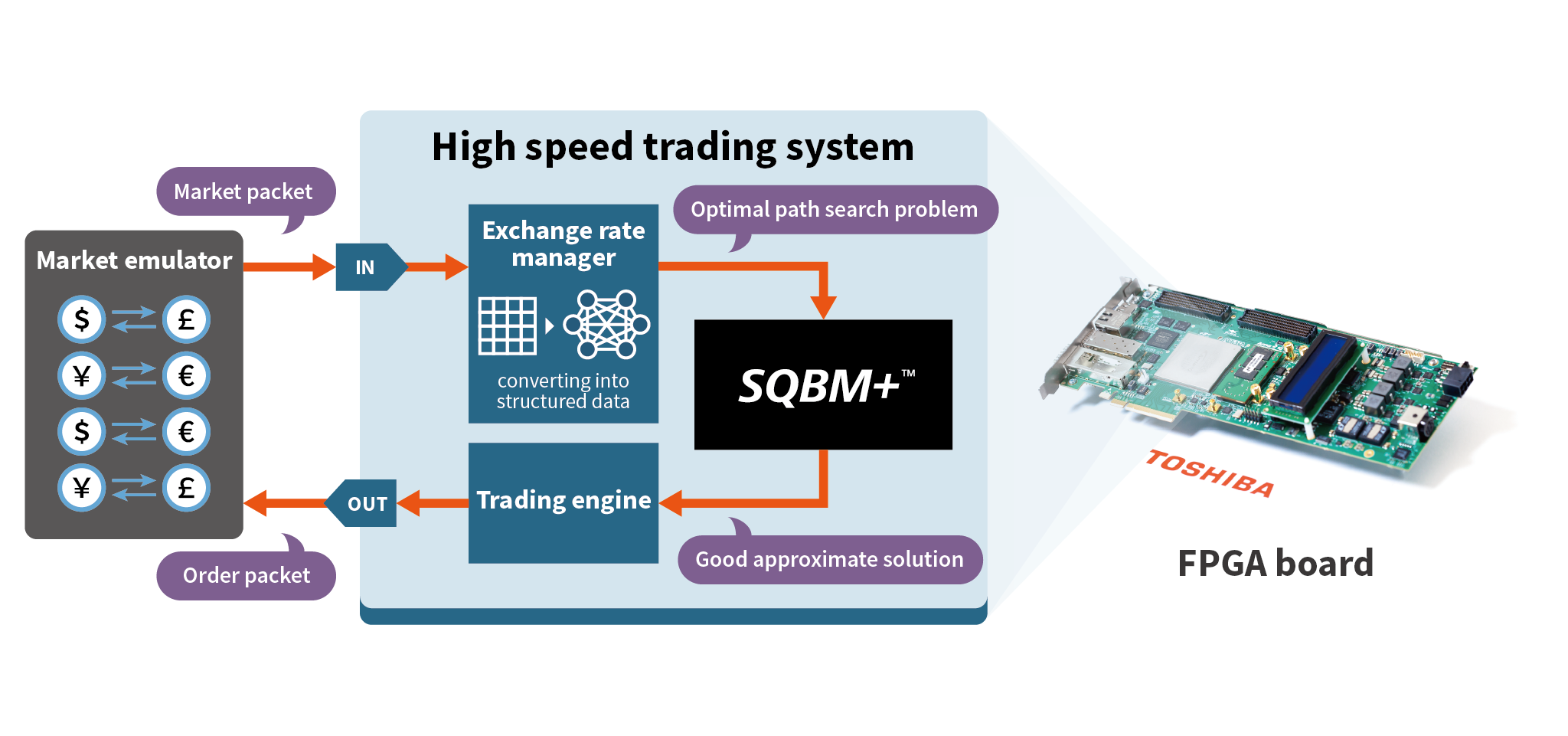

Currency-arbitrage HST is a method that takes advantage of the differences in exchange rates that occur only for a very short period of time, by circulating multiple currencies in transactions to generate profits.

Currency-arbitrage HST is a method that takes advantage of the differences in exchange rates that occur only for a very short period of time, by circulating multiple currencies in transactions to generate profits.

< 0.001sec

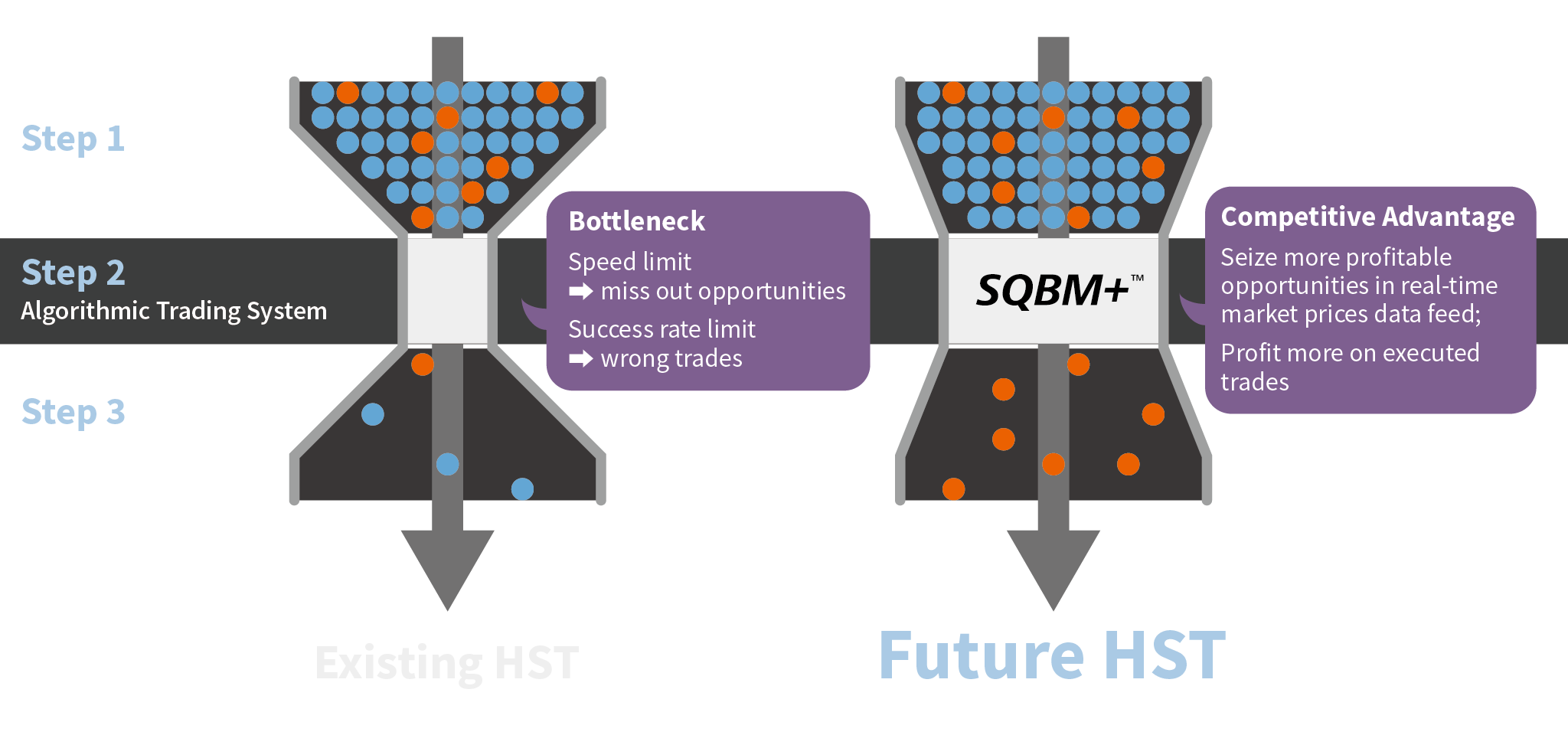

To complete a successful arbitrage cycle transaction, we must find a profitable currency exchange path and complete a trade within 1ms.

> 50%

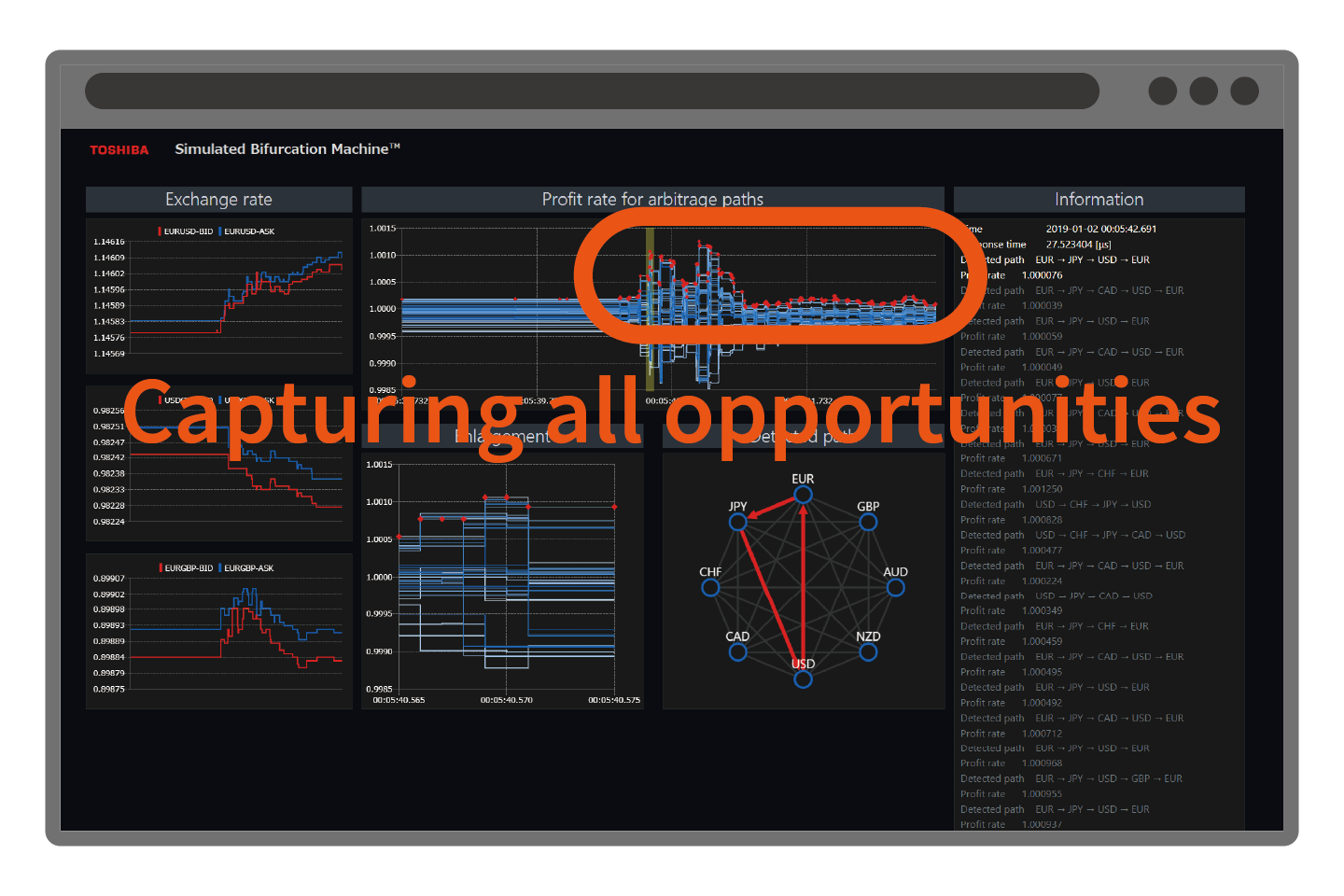

To maximize profit, we must discover as many profitable cycles as possible and execute only profitable trades.

*The percentage of identified (predicted) trading opportunities that prove to be true (profitable).

Resolve the algorithmic speed and success rate bottlenecks in HST, and build a huge competitive advantage

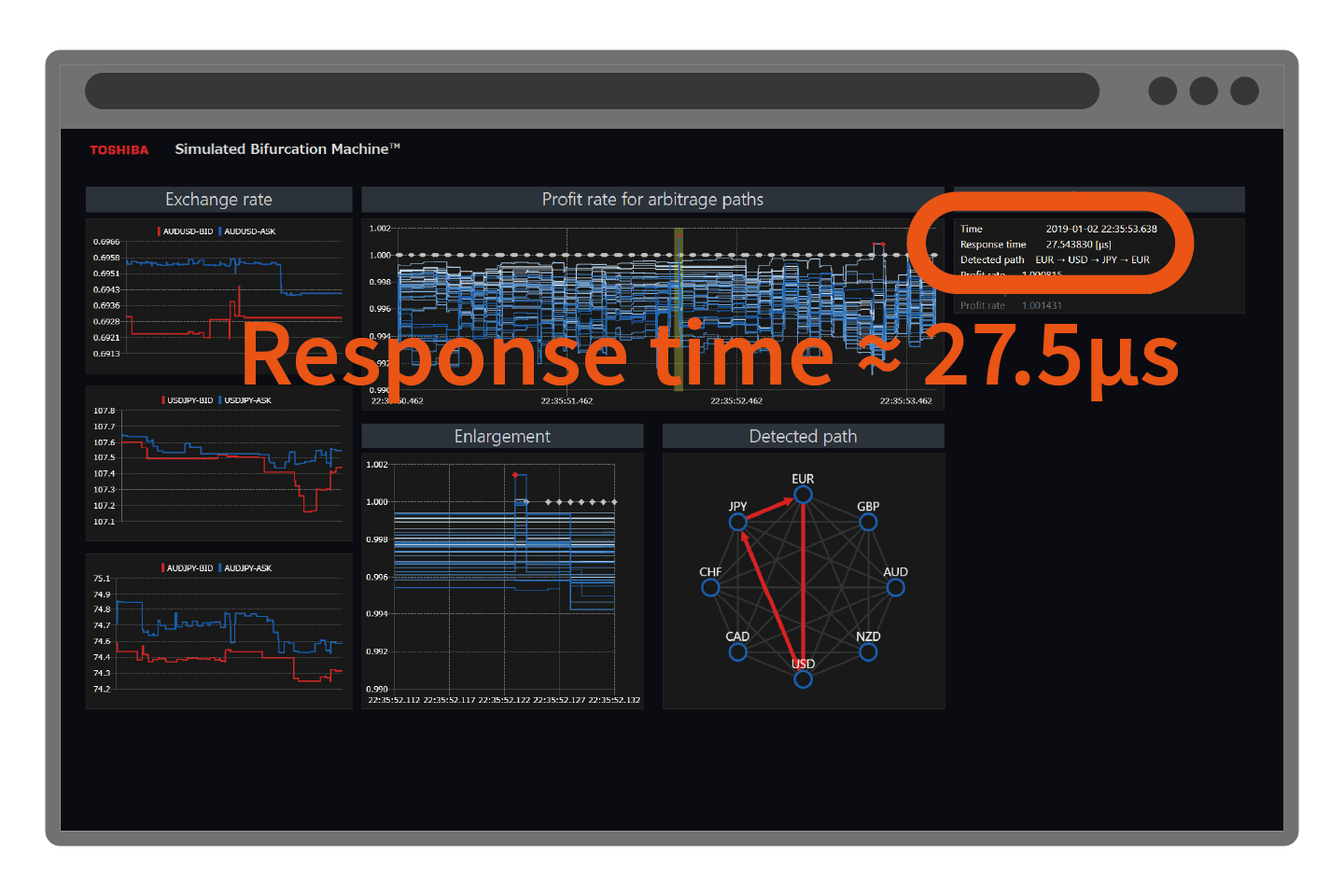

30μs

System-wide response time achieved, enabling the capture of opportunities within a sub-ms window

Seize More Opportunities

*μs=0.000001 seconds

98%

Trading accuracy achieved, enabling reliable profitability in real market environment

Greater Profitability and Reliability

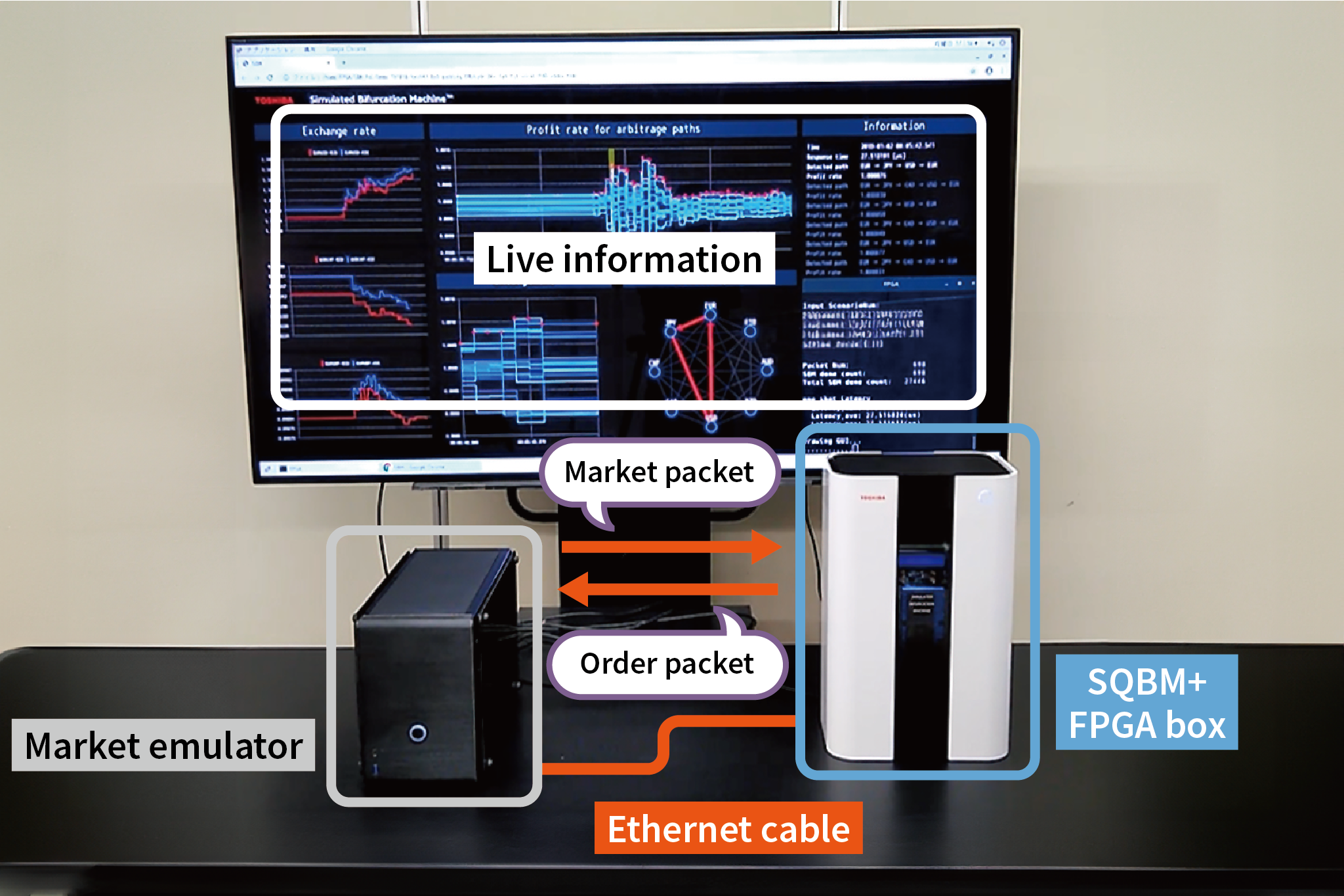

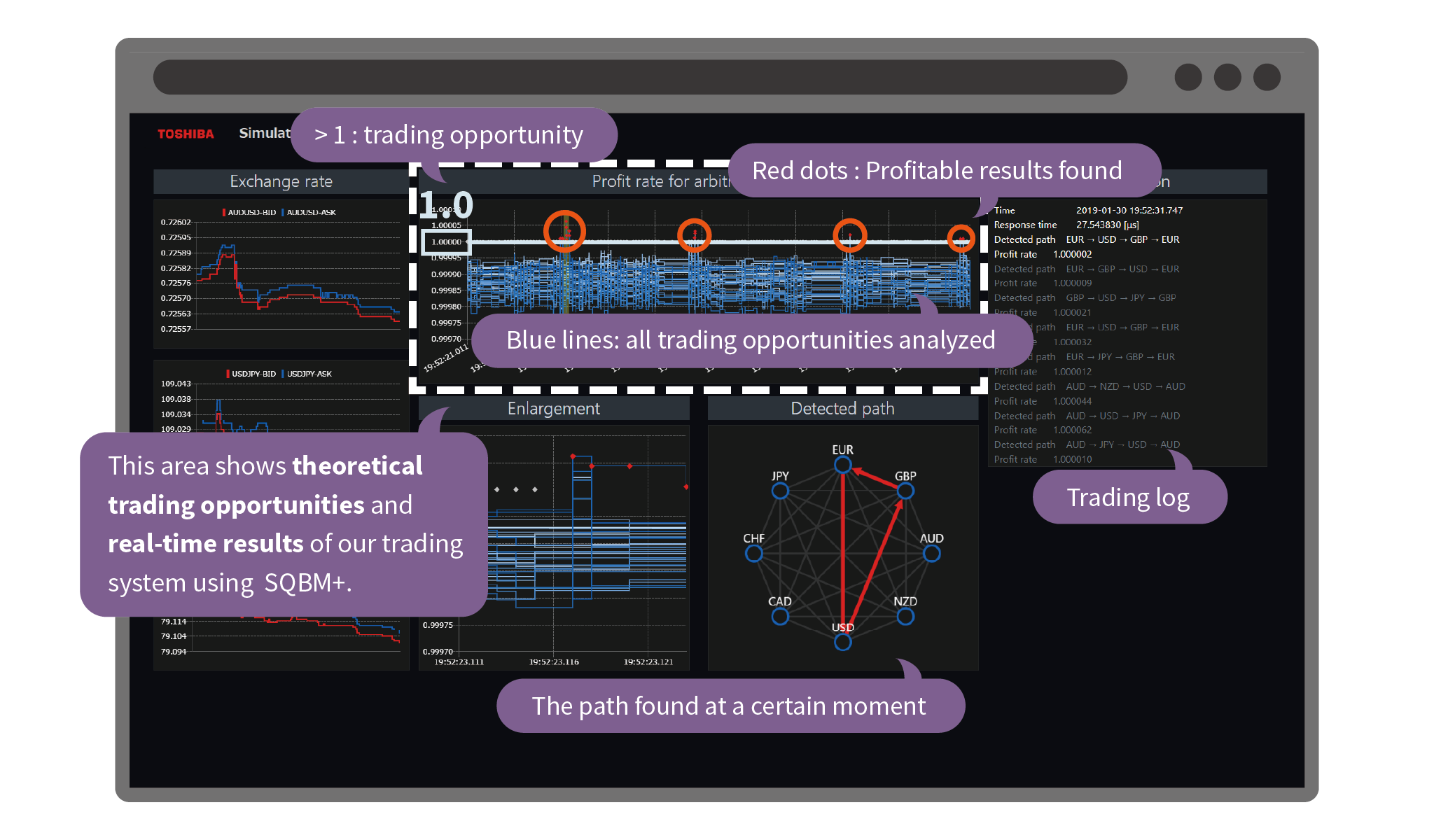

The online demonstration on the next page shows you how the HST finds the profitable opportunities by comparing the real-time results with the theoretical trading opportunities.

A very short-lived opportunity Captured

Multiple opportunities

in a time window

All captured without mistake

Support multiple currencies Flexible trading strategy

We conducted the demonstration of HST by connecting the SQBM+ system implemented on a FPGA board to a server that emulates real-time market prices data feed using historical data.